How to Select Mutual Funds Like an Expert: The Beginner`s Guide

Today, I will show you how to select the right mutual fund scheme —step by step and in a fun way.

Yeah, you read it right.

This topic is super important for anyone who invests in a mutual fund.

Yes, I know that’s why I am reading this blog. Come to the point directly.

Yes-Yes!

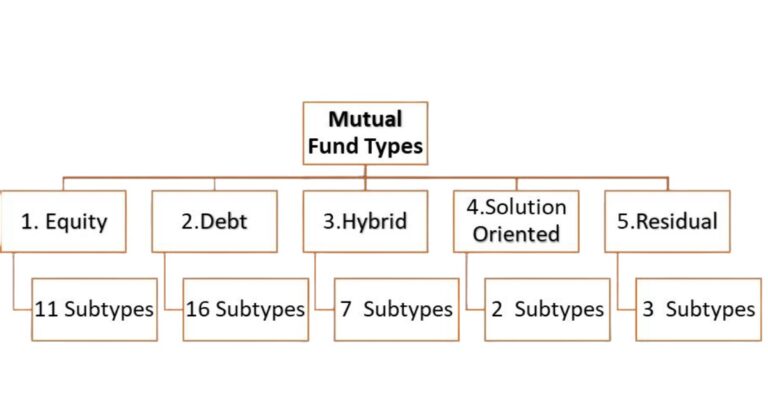

There are five different types of Mutual Funds. However, these five types have been further divided into 39 subtypes altogether. Moreover, around 2500 schemes run based on these 39 subtypes at any time. So, you have to pick a scheme from a pool of 2500.

Super confusing! Overwhelming! Boring!Boo!

I am not going to read any further.

Hey, do not run away. It is going to be super simple. I am not going to discuss these 2500 odd schemes anymore.

But you have to do a favour. So, please have a look at the below chart.

Now the most challenging part is over.

You need not know the details of these uncountable schemes. But you must know how to choose your favourite dish from the vast pool of buffets.

In this no-nonsense guide, I will show you how to choose your dish quickly and simply.

Ready to go! Let’s get started.

What is Mutual Fund Selection, Exactly?

For understanding, consider mutual funds as shirt fabric.

Now we can say that “Cotton”, “Silk”, “Woolen”, “Polyester”, “Handloom” are the five types.

And “Egyptian Cotton”, “Pima Cotton”, “100% Cotton”, etc. are the subtypes. So, in mutual funds, there are 39 subtypes in total.

Many brands sell each subtype of the shirt. In a mutual fund, there are around 45 brands known as “Asset Management Company” such as “ICICI Prudential“, “HDFC.”,” Mirae Asset Global“, “Axis“, “Sundaram“, “DSP.” etc. These brands sell their schemes based on these 39 subtypes. And, so there come the 2500 odd scheme.

Sorry! I again came back to these schemes and sub-schemes. But promise, it is over now.

The wrong way to select the Mutual Fund Schemes

Yes, the wrong way. And, this is the way you are most probably doing it. Initially, I was also selecting the mutual fund schemes in this way.

It is like going to a modern showroom (bank branches, some of the online portals or your so-called advisors who are, in reality, is mutual fund distributors) and asking for a shirt that suits you.

Now this salesperson or the senior manager, if you are wealthy enough, will judge your “pocket” and give you the best fund scheme, describing its expected benefits over the Bank F.D.

The important part is that he does not even measure your shoulder size, discuss specific fitting types ( slim or regular fit), or even bother to know the purpose like office wear or party wear.

Most of the time , he simply sells you that shirt (mutual fund schemes), which gives him the maximum commission.

Aha, you have invested in a Mutual fund.

Simple and hassle-free process!

I am not here to know the “Wrong ways of Mutual Fund Investment”. Come directly to the point and show me the “Correct Way”.

The Scientific and Right Way to Select the Mutual Fund Schemes:

You need to follow five steps to pick the right mutual fund scheme for you.

STEP1 # Know Your Financial Goal with a Timeline:

It means what sum of money and when you will require that money?

I guess your answer will be something like “maximum” and “as soon as possible”

But sadly, mutual funds do not work that way. Consequently, your financial goal needs to be S.M.A.R.T. Only then you will get success. But what is this S.M.A.R.T. ?

S.M.A.R.T. Financial Goal :

This means that your financial plan should be

Specific

Measurable

Achievable

Realistic

Time framed

The initial four points look pretty similar and theoretical. But the reality is quite the opposite. Let me explain to you with an example.

“Specific” here means things like “for my child’s wedding”, “for my retirement”, “for my child’s education”, “for my foreign vacation”, etc.

So, you must have a specific goal.

The “measurable” here means expressed in monetary units. For example, it could be “Rs. 5 crores”. However, it could not be like “sufficient or maximum money”.

The “Achievable” here means setting the goal, which is not very high. To clarify, you can not achieve a goal of accumulating Rs. 10 crores in 5 years by investing Rs. 10 per month.

Likewise, there is a difference between “achievable and realistic”. In the above example, as it is within your capacity to pay Rs.10 per month, it is realistic to assume that you will deposit this sum for 5 years, but your goal of Rs. 10 crores are not achievable.

In other words, the realisticity of a financial goal means the practical steps you will take to achieve that goal.

And the time frame is the simplest of all for the sake of understanding. This time frame is your “when” in the phrase “when you will need the money”.

When selecting a mutual fund scheme, you need to choose from the following time frame.

Short term (0-2 years)

Medium Term(2-5 years)

Long Term( more than 5 years)

So, knowing your SMART Financial goal is the first step towards selecting the type of mutual fund you need.

STEP2 # Know the Risk Involved in Achieving Your SMART Financial Goal

Mutual Fund investments carry a trade-off between risk and reward. If you’re willing to take more risk, you’ll have a greater chance of making money, but unfortunately, also a greater risk of losing it.

Every Mutual Fund type has a different level of risk involved. But there is one peculiarity about this risk.

Even the risk level of the same mutual fund scheme is different for everyone.

What is this? How can the same mutual fund scheme offer different levels of risk to another person?

I disagree.

O.k., Let me explain this to you.

The risk profile of an individual depends upon two things.

The risk-taking capacity of that individual, and

The risk tolerance nature. Tolerance is a subjective thing and a personality trait.

The risk capacity depends upon your income level, age, no. of dependents, family financial background, present wealth and debt etc.

The risk tolerance nature is your temperament. Even if there is a high-risk capacity, some people tend to take the minimal risk.

As the risk associated with the different mutual fund schemes vary, the decision should be based on your risk capacity and not on your temperament.

Just for fun, below are some of the famous dialogues of the movie made on the Harshad Mehta.

“Risk Hai Toh Ishq Hai”.

“Market me Sabse bada jokhim, jokhim na lene mein hai”.

STEP3 # Know the Fund Manager and its Track Record

The money you put in any mutual fund scheme is managed by the fund house or the AMC`s( Remember the 45 brands of our shirt or Asset management companies of mutual funds)

Moreover, the fund manager is the real guy who decides on behalf of all mutual fund investors of a particular scheme.

The scheme’s performance depends upon the expertise and decision of your fund manager. The fund manager is not the owner of the AMC but an employee. He has all the expertise to manage the total scheme investment amount. So, before selecting the mutual fund scheme, you must check the experience and track record of the fund manager.

STEP4 # Taxability Aspect of Mutual Fund Schemes

Your tax payable amount depends upon the type of mutual fund scheme as well as your holding period of that mutual fund scheme.

The taxation law also affects your actual return from a mutual fund. So, this aspect should also be looked upon while selecting mutual fund schemes.

They are ways to minimise taxation, and one must take advantage of the tax-saving avenues mentioned in the taxation act.

STEP5 # Expense Ratio of the Mutual Fund Scheme

You pay a fee to the mutual fund house for managing your money.

Really! But I have never paid this fee.

Fund management fees or expenses are deducted from the value of your investment. However, you may not be aware of it.

This expense ratio varies from scheme to scheme. It is also one of the parameters of mutual fund selection. If the high expense ratio of the fund is due to the high rate of commission to the mutual fund distributors, then this type of scheme should be discarded.

Also, the high expense ratio is a waste of money in the case of mutual fund schemes that depend on sensex and do not require fund managers active participation.

Conclusion:

Now you know the tested and proven way of selecting the right mutual fund schemes.

Is this the way you have been investing to date?

Do you know the average return of small-cap equity mutual funds in the year 2021?

It is a whopping 60% on average. Moreover, this is the average of the schemes taken together and not the maximum return of a particular scheme.

Yes, this type of mutual fund scheme is suitable for those with high-risk capacity and the “Risk Hai Toh Ishq Hai” type of temperament.

But you can afford to put at least some of your money in the high-risk category.

So, Mutual Fund Scheme selection is the most crucial aspect of your investment journey.

And, select a fund based on your financial objective, risk profile, fund manager track record, expense ratio, and personal tax benefits.

That’s all from my side. I hope you like my write up.

If you have any questions or doubts, click “Contact Me”, and we will meet over a zoom call/phone call to solve that confusion.